Metrics that Matter: How KPIs Define and Demonstrate Success

Publication Date: June 1, 2026

By Lisa Beymer and the ACUA Audit and Accounting Principles Subcommittee

While the term “Key Performance Indicator” (KPI) is not used in the Institute of Internal Auditor’s (IIA) revised Global Internal Audit Standards for considering the internal audit department’s effectiveness, it is clear that performance measurement is not optional. The underlying expectations call for internal audit functions to clearly define, monitor, and report on meaningful measures of performance. These measures are essential not only for demonstrating conformance to the Standards but also serve as objective evidence of Internal Audit’s effectiveness and value.

The following key Standards elevate the importance of performance measurement:

- Standard 8.3 requires the Chief Audit Executive (CAE) to maintain a quality assurance and improvement program that evaluates efficiency and effectiveness.

- Standard 8.4 has the expectation that external quality assessments evaluate whether the internal audit function is actively monitoring performance.

- Standard 9.2 requires supporting initiatives that align with Internal Audit’s strategy.

- Standard 12.2 specifically calls for developing objectives to measure performance.

Additionally, the IIA has released their IIA Performance Measurement Tool that provides guidance on conforming with Standard 12.2 on performance measurement.

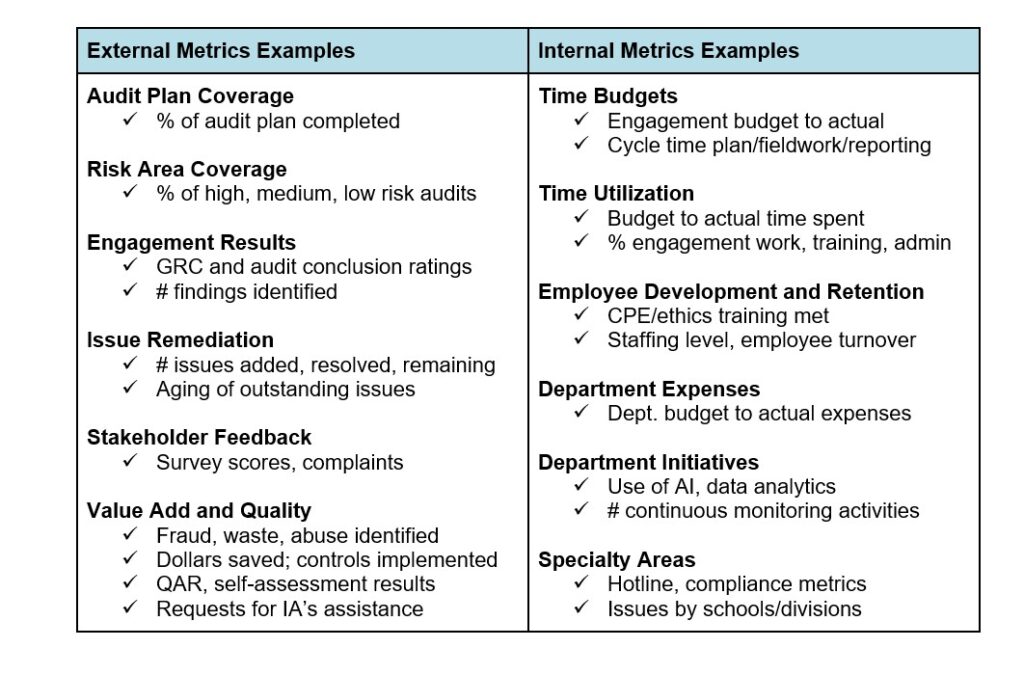

KPI Examples for Internal Auditors

Are your KPIs addressing the right risks and making a meaningful impact? Effective KPIs should directly align with your department’s strategy, areas of improvement needed, and stakeholder expectations. KPIs can also be internal or external – designed for the benefit of the internal audit shop or to furnish outside leadership with performance information.

Measuring Activity and Value in Thoughtful KPI Design

Take your KPIs even farther by tying them to goals to drive positive action rather than simply reporting activity. Rather than only reporting the quantity of engagements completed during the year, set a desired completion rate as a goal. For example, “we completed 18 of 20 planned engagements,” can be tied to a goal by stating “we completed 90% of our planned audits, which exceeds our goal of 85%.”

Make sure your goals are SMART – specific, measurable, achievable, relevant, and timely. For example, a goal to “decrease time spent in reporting” can become a SMART goal by adding details, such as “decrease average days spent in reporting from 45 to 30 by the end of this calendar year.”

Monitoring KPIs can be achieved using the simplest of manual Excel spreadsheets to embedded dashboards and modules from audit workpaper management software. Progress on KPIs is often shared with senior management and the board through annual reports and board presentations.

The Double-Edged Sword of KPIs

Well-designed KPIs drive quality, accountability, and continuous improvement. On the other hand, poorly designed or managed KPIs can encourage shortcuts, misaligned priorities, or even unintended manipulation. For example, overly emphasizing a shorter audit cycle time could lead to rushed fieldwork. Encouraging a high number of audit findings could lead to auditors making mountains out of molehills, which may negatively affect your department’s credibility.

There are numerous challenges to developing a KPI system. The ability to gather and update data from multiple sources can be time consuming, and data reliability may become a factor. There is a risk of only measuring the activity versus its impact. KPI results may be misinterpreted by management, and CAEs may be tempted to skew the statistics to appear more favorable. Additionally, the audit team may be reluctant to adapt to new goals.

When creating balanced and relevant KPIs, consider the following practical implementation tips:

- Measure what is most meaningful, not just what is easiest to track.

- Focus on outcomes, not just activity.

- Define KPIs clearly to avoid confusion in how they are measured.

- Avoid KPI overload – keep the team focused on the metrics that matter most.

- Be balanced – include multiple dimensions of performance measurement.

- Involve the team to promote accountability and buy-in.

- Periodically review KPIs to ensure they are not outdated or irrelevant.

Well-defined KPIs can improve the audit department’s effectiveness and efficiency while addressing the new Global Internal Audit Standards. With the new fiscal year approaching, this is a great time to evaluate and enhance your department’s KPIs.

About the Author

The Auditing & Accounting Principles Subcommittee is dedicated to keeping the ACUA membership informed about changes to applicable auditing and accounting standards and developing tools and resources for members. This article was adapted from a presentation at the ACUA Virtual Spring Summit on March 26, 2028, by presenters:

- Hollie Andrus, University of Utah

- Lisa Beymer, Indiana University

- Patty Davidson, SUNY Binghamton

- Kara Hefner, University of North Carolina, Chapel Hill