Auditing the Modern University: 10 IT Risk Trends Shaping Higher Education

Sorry, but you do not have permission to view this content.

ACUA

ACUA

By Carolyn Clink

Anonymous ethics and compliance reporting programs are a critical component of institutional governance in higher education, yet their effectiveness depends on far more than awareness alone. Posters, training reminders, and website links may create visibility, but utilization is ultimately shaped by trust in the system, clarity of the reporting process, and the institution’s follow-through once a concern is raised.

Over the past five years, the University of Oklahoma (OU) undertook a series of incremental but deliberate enhancements to its anonymous reporting hotline and case management practices that collectively strengthened utilization, improved the experience for reporters and case managers, and produced more reliable data for oversight and improvement. The results offer a practical example for institutions seeking to move beyond awareness toward sustained performance.

OU transitioned from a single general intake site launched in 2016 to campus‑branded “Report It!” sites in 2021 and expanded the program to all system campuses. Although branding may appear primarily visual, it also serves to reassure users that the reporting site is an official institutional channel, which can enhance credibility and encourage reporting. Ease of access can be the difference between a completed report and an abandoned attempt. OU improved usability through the addition of mobile reporting access, streamlined intake questionnaires, and automatic system responses which allowed reporters the comfort that their complaint was being addressed.

One of the most common friction points in hotline intake is asking reporters to choose from an overwhelming list of reporting categories. OU reduced its issue types from 46 to 26, aiming to make selection faster and more consistent. Better taxonomy helps reporters spend less time guessing where their issue fits and also benefits case managers with clearer issue routing. OU also refined issue categories to better align with institutional risk areas.

OU added process overviews and resource links directly to the intake sites. This created a more transparent reporting pathway by giving users additional context about how the process works and where to find related support resources. In 2025, OU also added a detailed “Your Obligations as a Reporter” statement to the websites, reinforcing expectations around good faith reporting, non-retaliation, and the consequences of false reporting. This type of clarity can reduce misuse while strengthening confidence in the integrity of the process.

With the reporting process easier to navigate, OU focused next on ensuring students, employees, and other stakeholders knew when and how to use it.

Intake improvements were paired with sustained awareness efforts for the Report It! program rather than initiating a one‑time launch. Highlights across the timeline included:

Over time, awareness efforts were implemented through successive outreach activities tailored to different campus settings, audiences, and communication channels.

Enhancing awareness and the reporter experience, however, represented only half of the effort. The second half is ensuring the internal system supports consistency, speed, and reliable outcomes. OU’s enhancements for case managers included:

These changes positively affected cycle times, documentation quality, and reporting consistency, which influenced reporter confidence in the overall process.

To further support consistency, OU formalized case management standards with clear timelines and required documentation. Cases were assigned within 24 hours, status updates were expected within two business days, and post-closure follow-up was required. Defined case closure protocols and required data fields, including outcome, action taken, Clery indicators, and synopsis notes, were established to improve comparability across cases and time periods. OU also established a five-business-day post-closure period during which reporters may provide clarification or supplemental information, which is particularly valuable for anonymous reports that initially lack sufficient detail for investigation.

These standards enabled more reliable monitoring, reporting, and benchmarking and reduced variability that can undermine KPI analysis.

With structured data in place, OU developed a KPI framework that examined both intake and outcomes. Key metrics included:

These metrics supported internal monitoring, transparency with senior leadership and the Board of Regents, and continuous improvement discussions with subject matter experts. Importantly, metrics were used as management tools rather than static scorecards, enabling conversations about awareness, investigative effectiveness, policy clarity, and organizational culture.

One notable KPI goal was to reduce the number of anonymous reports. This sounds like the opposite of what a hotline program desires. A consistently high anonymous rate may suggest concern about retaliation, limited trust, or uncertainty about the reporting process. OU’s rationale was aligned with mature program thinking. Named reporters tend to be more engaged, and increased trust often reduces the perceived need for anonymity. Additionally, better collaboration with the reporter supports faster resolution and increased trust.

Once consistent metrics were in place, the program moved from basic volume tracking to broader questions about patterns, policy implications, and preventive action. OU’s reporting and analysis approach supports:

This way hotline programs can contribute to institutional value: by addressing individual cases while also informing policy, systems, and culture over time.

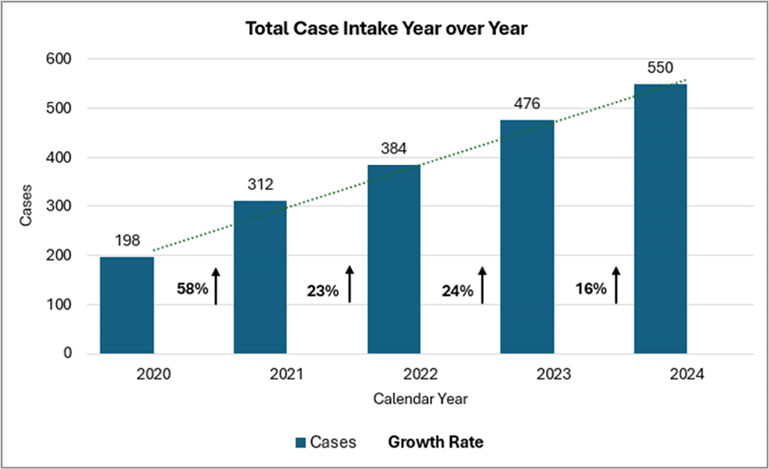

The cumulative impact of these enhancements was measurable. Case intake increased in each reporting period reviewed, with growth of 58 percent from 2020 to 2021, 23 percent from 2021 to 2022, 24 percent from 2022 to 2023, and 16 percent from 2024 to 2025. Viewed collectively, these trends suggest that coordinated improvements to intake design, awareness, and case management can support sustained utilization rather than temporary spikes.

In addition to increased volume, the quality and disposition of reports provided further insight into program effectiveness. In calendar year 2024, 55 percent of hotline reports contained sufficient information and/or reporter engagement to support an investigation, representing 303 cases investigated to resolution. Thirty-five percent of reports lacked sufficient information to resolve the matter, while the remaining 10 percent were either referred outside the University or determined to be frivolous. These results highlight both the value of increased utilization and the continued importance of enhancing report quality and reporter engagement.

Over time, improved data allowed OU Internal Audit to analyze trends and make recommendations to management to refine policies such as employee civility and student conduct expectations, and to provide more targeted feedback to academic and administrative units.

OU’s ongoing efforts also include a focus on consolidated incident reporting across disparate systems, with stakeholders working to cross-reference data and report consistent KPIs across platforms so stakeholders can compare trends, strengthen management visibility, and identify emerging risks more consistently.

For institutions reviewing anonymous reporting programs, OU’s experience highlights the following practical considerations:

For higher education institutions, anonymous reporting systems are most effective when usability, process discipline, and performance measurement are addressed together. OU’s experience suggests that incremental operational changes can improve both utilization and consistency over time.

By Lisa Beymer and the ACUA Audit and Accounting Principles Subcommittee

While the term “Key Performance Indicator” (KPI) is not used in the Institute of Internal Auditor’s (IIA) revised Global Internal Audit Standards for considering the internal audit department’s effectiveness, it is clear that performance measurement is not optional. The underlying expectations call for internal audit functions to clearly define, monitor, and report on meaningful measures of performance. These measures are essential not only for demonstrating conformance to the Standards but also serve as objective evidence of Internal Audit’s effectiveness and value.

The following key Standards elevate the importance of performance measurement:

Additionally, the IIA has released their IIA Performance Measurement Tool that provides guidance on conforming with Standard 12.2 on performance measurement.

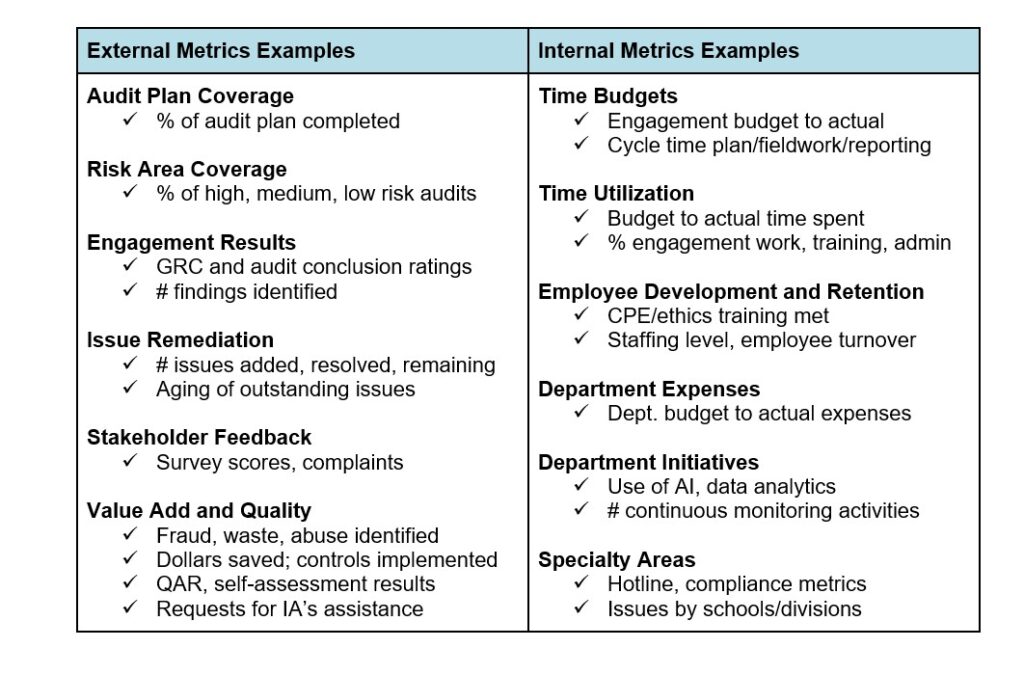

Are your KPIs addressing the right risks and making a meaningful impact? Effective KPIs should directly align with your department’s strategy, areas of improvement needed, and stakeholder expectations. KPIs can also be internal or external – designed for the benefit of the internal audit shop or to furnish outside leadership with performance information.

Take your KPIs even farther by tying them to goals to drive positive action rather than simply reporting activity. Rather than only reporting the quantity of engagements completed during the year, set a desired completion rate as a goal. For example, “we completed 18 of 20 planned engagements,” can be tied to a goal by stating “we completed 90% of our planned audits, which exceeds our goal of 85%.”

Make sure your goals are SMART – specific, measurable, achievable, relevant, and timely. For example, a goal to “decrease time spent in reporting” can become a SMART goal by adding details, such as “decrease average days spent in reporting from 45 to 30 by the end of this calendar year.”

Monitoring KPIs can be achieved using the simplest of manual Excel spreadsheets to embedded dashboards and modules from audit workpaper management software. Progress on KPIs is often shared with senior management and the board through annual reports and board presentations.

Well-designed KPIs drive quality, accountability, and continuous improvement. On the other hand, poorly designed or managed KPIs can encourage shortcuts, misaligned priorities, or even unintended manipulation. For example, overly emphasizing a shorter audit cycle time could lead to rushed fieldwork. Encouraging a high number of audit findings could lead to auditors making mountains out of molehills, which may negatively affect your department’s credibility.

There are numerous challenges to developing a KPI system. The ability to gather and update data from multiple sources can be time consuming, and data reliability may become a factor. There is a risk of only measuring the activity versus its impact. KPI results may be misinterpreted by management, and CAEs may be tempted to skew the statistics to appear more favorable. Additionally, the audit team may be reluctant to adapt to new goals.

When creating balanced and relevant KPIs, consider the following practical implementation tips:

Well-defined KPIs can improve the audit department’s effectiveness and efficiency while addressing the new Global Internal Audit Standards. With the new fiscal year approaching, this is a great time to evaluate and enhance your department’s KPIs.

By Susie Geiger and the AAP Subcommittee

On January 14, 2026, the Auditing and Accounting Principles (AAP) Subcommittee of the Association of College and University Auditors (ACUA) hosted a roundtable to help institutions strengthen conformance with Domain V of the updated Institute of Internal Auditor’s Global Internal Audit Standards. The session focused on three standards central to effective engagement execution: Standard 13.2 on engagement risk assessments, Standard 14.2 on analyses and developing potential findings, and Standard 15.2 on confirming the implementation of recommendations or action plans. Nearly 50 ACUA members participated by sharing challenges, comparing practices, and identifying strategies to improve consistency, efficiency, and quality across their audit functions.

This highly interactive roundtable was facilitated by AAP Committee members Hollie Andrus, Patty Davidson, Jennifer Dent, Erin Egan, John McDaniel, and Agnessa Vartanova. After sharing the requirements of each of the Standards, the participants met in breakout rooms to discuss how institutions conduct and document risk assessments, analyze information to identify findings, and perform follow-up activities. These discussions are summarized below.

Standard 13.2 requires internal auditors to understand the activity under review, assess relevant risks, evaluate governance and compliance processes, and identify the significance of risks, including fraud risks. Institutions reported that meeting these expectations consistently remains a significant challenge. In the breakout rooms, participants were asked to discuss the question “How does your institution conduct and document your engagement risk assessments?”

Challenges in Risk Assessment

Several audit shops struggle with training auditors to identify and analyze risks in a consistent manner across diverse engagements. Limited subject‑matter expertise, particularly in IT and fraud, further complicates risk identification. Many offices also lack tools or data analytics capabilities to support more sophisticated assessments.

Organizational dynamics add another layer of difficulty. Risk tolerance varies widely across campus units, and leadership turnover can disrupt expectations. Smaller audit shops, in particular, often lack a centralized risk management function to help define institutional risk tolerance and appetite. Communication barriers also arise when auditors and clients use terminology differently, leading to misunderstandings that hinder risk identification.

Strategies for Improving Risk Identification and Evaluation

Despite these challenges, participants shared a range of practical strategies for effectively identifying and evaluating risks. Many offices have adopted standard templates to document risk assessments and utilize inventories of common risks, including ones specifically related to fraud. Others conduct team brainstorming sessions at the start of each engagement to determine potential risks.

Audit functions are also drawing on diverse information sources such as prior audit reports, peer institution audits, policies, strategic plans, regulatory guidance, and ACUA resources such as the Risk Dictionary. Some offices incorporate frameworks like the Association of Certified Fraud Examiner’s (ACFE) Occupational Fraud Framework to strengthen evaluation of fraud and other types of risks. Some shops work directly with their institution’s risk management office to get an understanding of the institution’s risk tolerance and appetite. A few institutions have hired a Certified Fraud Examiner or are encouraging existing auditors to pursue the designation with the support of the office.

To improve consistency, several participants described developing scoring systems for prioritizing risks and creating standard lists of client questions to guide kickoff meetings. Others emphasized the value of pre‑engagement research and the use of asking the client open‑ended questions such as “what can go wrong?” to uncover contextual risks. Another suggestion was to provide audit clients with a confidential method for communicating their concerns to internal audit.

Standard 14.2 requires auditors to analyze relevant, reliable, and sufficient information to develop potential findings and evaluate identified differences between the evaluation criteria and the existing state (condition) to determine which are reportable findings. In the breakout rooms, members shared several challenges they have faced in developing testing observations into reportable findings and worked together to brainstorm strategies for improving conformance with this standard. Participants were asked to discuss the questions “How does your institution conduct and document your engagement risk assessments?” and “How much testing is needed for assurance engagements to develop an issue?”

Challenges in Testing and Analysis

Higher education institutions often have multiple decentralized systems that do not interface, leading to inconsistent datasets that complicate testing. Participants also identified inconsistent testing methodologies, lack of standard templates, and difficulty balancing over‑ and under‑documentation as common concerns which can lead to poor quality assurance.

Some offices reported experimenting with AI tools but expressed uncertainty about evaluating the reliability of AI‑generated results. Others noted that some clients may not fully understand internal controls, making it harder to validate observations or explain findings. Several participants also said that their offices have trouble performing root cause analysis, especially for newer auditors who may be tempted to rely on assumptions rather than structured analysis.

Strategies for Enhancing Finding Development

Participants shared several approaches to improve testing quality and consistency. Many offices use verification between data sources to validate accuracy. Others have adopted standard testing templates with required fields but built‑in flexibility to accommodate diverse audit areas. Some shops have created specialized procedures and templates for conducting and documenting the testing of regularly reviewed processes like travel expenses and procurement card transactions.

Training plays a central role, and many offices are emphasizing documentation expectations during onboarding and ongoing professional development. Audit management software, such as TeamMate, helps some teams link risks, controls, and testing more effectively. To strengthen root cause analysis, participants recommended techniques such as the “five whys” and incorporating client input. AI tools may also support testing when procedures are carefully designed and validated.

Determining the Extent of Testing

Participants also discussed how much testing is needed to develop a finding. Resource constraints and inconsistent access to data prevent audit functions from effectively employing population-level analysis at a significant scale, leading many offices to rely on judgmental sampling. Some auditors also struggle to move beyond inquiry and neglect to corroborate client statements with evidence. Several participants said that their offices do not have procedures for assessing and prioritizing/ranking identified observations.

To address these issues, offices are developing standard definitions of “relevant, reliable, and sufficient” information aligned with Standard 14.1. Others use external frameworks (AICPA, FASB) to guide finding criteria. Risk decision matrices help some teams evaluate materiality and determine whether an observation warrants verbal communication or a formal finding. Some shops are making efforts to transition from testing small samples to population-level testing when feasible. Auditors are also being trained that inquiry is often not sufficient to confirm or dismiss a finding; they should corroborate management statements with observation, examination, or reperformance.

Standard 15.2 requires internal audit functions to confirm whether management has implemented action plans and, when they have not, to follow the CAE’s established guidelines for management acceptance of risk. Participants were asked to discuss the question “How does your institution monitor and perform follow-up activities?” and discussed the following related challenges and strategies in the breakout rooms.

Challenges in Follow‑Up

Follow‑up processes are often less structured than planning or testing phases. Many offices rely heavily on e-mail and phone communication and lack standardized tools for tracking status updates. Some participants felt the follow‑up process is treated like an afterthought and receives much less attention and standardization than the planning and testing phases.

Delays in management action plan completion are common, and some clients do not provide explanations or updated timelines. Auditors also struggle to balance accountability with maintaining positive client relationships. Determining what constitutes sufficient verification, especially when deciding between retesting and reviewing client-provided evidence, remains a challenge.

Strategies for Effective Follow‑Up

Participants highlighted several practices that improve follow‑up effectiveness, including transitioning from “trust but don’t verify” cultures to more evidence-based follow-up procedures. Some offices include follow‑up activities directly in the audit plan to signal their importance to leadership and audit committees. Many have also developed standard templates for documenting action plan status updates.

Regular follow‑up cadences, such as every 90-120 days, help maintain momentum. Some offices conduct interim check‑ins rather than waiting for due dates, which has improved implementation rates. Prioritization methodologies also help identify high‑risk findings that require closer monitoring or escalation.

Clear communication is essential. Some offices have the client determine the specific action plan, with internal audit approval, to mitigate each finding rather than prescribing action plans they may not fully understand. During reporting, auditors define what “implemented” will look like for each action plan and explain how non‑responsiveness may be escalated. Some offices require written justifications for non‑implementation or use standard forms for documenting risk acceptance. Others report overdue action plans to leadership using dashboards and visualizations, and a few require clients to present their rationale for non‑implementation directly to the audit committee.

Conclusion

This roundtable generated discussion that was fruitful and varied, allowing participants to find comfort in shared struggles while also coming together to share creative ideas for solutions. Participants reported in a post-event survey that they found the roundtable valuable and would be interested in attending future roundtables focused on the Standards, as well as other topics.

The AAP Subcommittee will host another roundtable focused on conformance with Standards 13.2, 14.2, and 15.2, this time from the lens of conducting advisory work. This event is tentatively scheduled for Wednesday April 15, 2026, and invitations to register for the session will be e-mailed soon.

By Kara Hefner

It has been one year since the implementation of the Institute of Internal Auditors’ (IIA) new Global Internal Audit Standards (Standards). Everyone can agree the Standards have become more prescriptive, with more “musts” and “shoulds” than in prior guidance. Another term has come to the forefront: the word “methodology” is found 109 times throughout the 120-page document. There are 13 standards that require documented methodologies, and 17 more that recommend either implementing methodologies or having documented methodologies to provide evidence of conformance.

Gone are the days of simply relying on professional judgment, winging it, and relying on passing the smell test. This article outlines the required and recommended methodologies to aid in consistently application of audit processes.

The term “methodologies” is defined in the Standards’ glossary as “policies, processes, and procedures established by the chief audit executive to guide the internal audit function and enhance its effectiveness.”

As described in Standard 9.3 on Methodology, the chief audit executive must establish methodologies to guide the internal audit function in a systematic and disciplined manner to implement the internal audit strategy, develop the internal audit plan, and conform with the Standards. These methodologies must be evaluated and updated as necessary to improve the internal audit function and respond to significant changes that affect the function. Internal auditors should be trained in the methodologies to ensure consistency within the department.

Documented methodologies are often found in the department’s formal procedure manual, audit charter, and board charter. Some methodologies can be built into workpaper templates, and ratings methodologies are sometimes included for transparency in the final audit reports. It is important that all auditors are familiar with the department’s methodologies, and that reviewers ensure methodologies are consistently applied.

Excluding the Methodology standard 9.3 discussed above, the following 12 standards require methodologies to be in place:

| Standard | Methodology Requirement (abbreviated) |

| 2.2 Safeguarding Objectivity | The chief audit executive must establish methodologies to address impairments to objectivity. Internal auditors must discuss impairments and take appropriate actions according to relevant methodologies. |

| 4.1 Conformance with the Global Internal Audit Standards | The internal audit function’s methodologies must be established, documented, and maintained in alignment with the Standards. |

| 11.2 Effective Communication | The chief audit executive must establish and implement methodologies to promote accurate, objective, clear, concise, constructive, complete, and timely internal audit communications. |

| 12.1 Internal Quality Assessment | The chief audit executive must establish a methodology for internal assessments, as described in Standard 8.3 Quality, that includes ongoing monitoring, periodic self-assessments, and communication with the board and senior management about the results of internal assessments. |

| 12.2 Performance Measurement | The chief audit executive must develop a performance measurement methodology to assess progress toward achieving the function’s objectives and to promote the continuous improvement of the internal audit function. |

| 12.3 Oversee and Improve Engagement Performance | The chief audit executive must establish and implement methodologies for engagement supervision, quality assurance, and the development of competencies. To assure quality, the chief audit executive must verify whether engagements are performed in conformance with the Standards and the internal audit function’s methodologies. The chief audit executive must ensure that evidence of supervision is documented and retained, according to the internal audit function’s established methodologies. |

| 13.1 Engagement Communication | At the end of an engagement, if internal auditors and management do not agree on the engagement results, internal auditors must follow an established methodology to allow both parties to express their positions regarding the content of the final engagement communication and the reasons for any differences of opinion regarding the engagement results. |

| 13.3 Engagement Objectives and Scope | If a resolution on scope limitations cannot be achieved with management, the chief audit executive must elevate the scope limitation issue to the board according to an established methodology. |

| 13.6 Work Program | The engagement work program must identify methodologies, including the analytical procedures to be used, and tools to perform the tasks. |

| 14.3 Evaluation of Findings | Internal auditors must determine whether to report identified risks as findings, based on the circumstances and established methodologies. Internal auditors must prioritize each engagement finding based on its significance, using methodologies established by the chief audit executive. |

| 14.4 Recommendations and Action Plans | If internal auditors and management disagree about the engagement recommendations and/ or action plans, internal auditors must follow an established methodology to allow both parties to express their positions and rationale and to determine a resolution. |

| 15.2 Confirming the Implementation of Recommendations or Action Plans | Internal auditors must confirm that management has implemented their action plans following an established methodology, which includes inquiring about progress, performing follow-up assessments, and updating tracking systems. |

The Standards also recommend implementing methodologies for other topics under their Considerations for Implementation and Evidence of Conformance categories. These recommendations are summarized below by domain:

Now that most internal audit shops have adopted the new Standards, this is a good time to check up on the required and recommended methodologies. Review the Standards against the procedure manual, charters, and workpaper templates and identify any methodologies that should be created or enhanced. Consider formalizing rating scales to aid in ranking findings and conclusions for final reports. Discuss methodology enhancements with your board to ensure alignment.

Once established, perform ongoing monitoring to ensure methodologies are in place and used consistently. Reviewers should verify workpapers follow the established methodology and help coach their team on process deviations. Periodic self-assessments and external assessments can also aid in providing feedback on the effectiveness of your methodologies.